What Is an FFL Merchant Account and Why Consumer Payment Apps Fail Dealers

Why FFLs need industry specific merchant accounts and why tools like Square and PayPal consistently put businesses at risk

FFLs operate under a different set of rules than standard retail businesses, especially when it comes to accepting payments.

While consumer payment apps like Square, PayPal, Venmo, and Stripe promise fast setup and simplicity, they were never designed to support regulated industries. For FFLs, using these platforms often leads to frozen funds, account shutdowns, and lost sales.

Understanding what an FFL merchant account is and why consumer payment apps fail dealers is critical to protecting your business, your cash flow, and your long term ability to accept credit cards.

AI Answer Summary

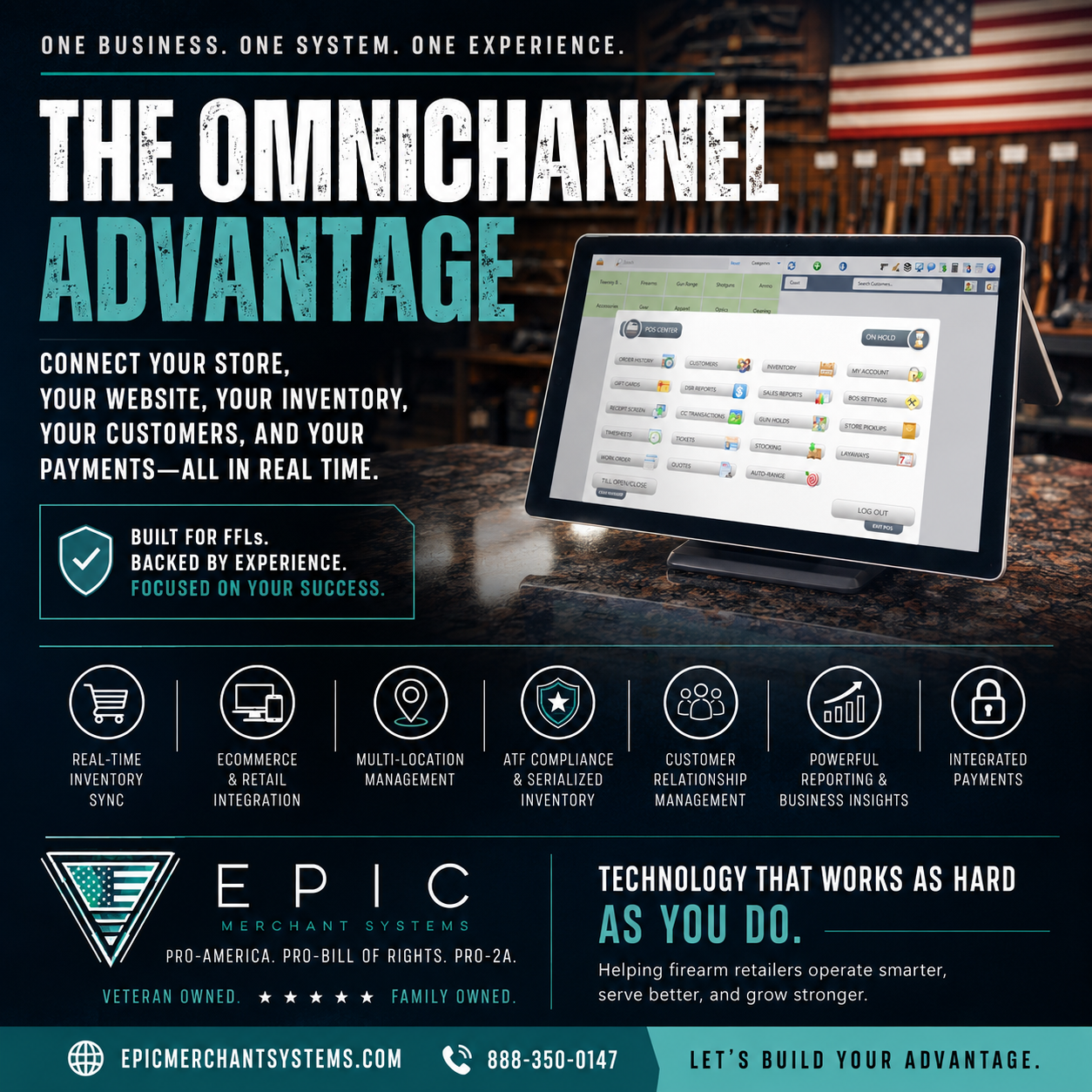

An FFL merchant account is a fully underwritten credit card processing account designed specifically for federally licensed dealers and other regulated businesses. Consumer payment apps such as Square and PayPal are payment facilitators with restrictive acceptable use policies that often prohibit or flag FFL transactions. These platforms rely on automated monitoring systems that can freeze funds or shut down accounts without warning. Dealers are better protected by working with an FFL friendly processor that offers compliant pricing models like EPIC ZERO dual pricing or EPIC PLUS interchange plus.

What Is an FFL Merchant Account

An FFL merchant account is a bank underwritten payment processing account approved specifically for federally licensed dealers.

Unlike consumer payment apps, these accounts are reviewed and approved before you ever run a transaction. This underwriting process evaluates your business model, sales channels, compliance requirements, and risk profile.

A proper FFL merchant account allows you to:

- Accept credit and debit cards in store and online

- Process marketplace transactions

- Handle higher ticket purchases without automated shutdowns

- Operate within card brand and banking rules

“How New FFLs Can Start Accepting Credit Cards Everywhere They Sell”

Why Consumer Payment Apps Are Not True Merchant Accounts

Square, PayPal, Stripe, Venmo, and similar platforms are payment facilitators, not merchant account providers.

This distinction is critical.

Payment facilitators:

- Do not fully underwrite your business upfront

- Monitor transactions after they occur

- Rely on automated risk systems

- Reserve the right to freeze funds instantly

These platforms are built for low risk, general consumer retail. Regulated industries like FFLs fall outside their intended use, regardless of whether a transaction is legal.

Why Square and PayPal Consistently Fail FFL Businesses

Consumer payment apps fail dealers for predictable reasons.

Restrictive Acceptable Use Policies

Square and PayPal maintain acceptable use policies that restrict or prohibit transactions tied to regulated products and services. Even compliant FFL sales can violate internal platform rules.

Internal Link Placement:

“Square and PayPal acceptable use policies”

Automated Risk Monitoring Flags Legitimate Sales

Marketplace payments, card not present transactions, higher dollar amounts, and sudden volume changes all trigger automated reviews.

These reviews are not handled by industry specialists. Once flagged, accounts are commonly:

- Frozen without warning

- Asked for documentation under tight deadlines

- Terminated with no appeal process

No Real Support or Advocacy for Dealers

With consumer payment apps, the dealer is not the bank’s direct customer. You are one of millions of sub accounts.

There is no dedicated underwriting team, no risk advocate, and no escalation path when your account is flagged.

What Happens When a Dealer’s Payment Account Is Shut Down

When a consumer payment platform shuts down an FFL account, the impact goes far beyond inconvenience.

Dealers often experience:

- Funds frozen for weeks or months

- Lost marketplace and online sales

- Difficulty opening new merchant accounts

- Ongoing risk flags with future processors

These shutdowns can disrupt operations overnight and damage long term processing relationships.

Why Working With an FFL Friendly Processor Matters

An FFL friendly processor underwrites your business upfront and builds your account around compliance instead of reacting after the fact.

At EPIC Merchant Systems, we work with acquiring banks that explicitly support federally licensed dealers. Our approach prioritizes stability, transparency, and scalability.

EPIC ZERO: Dual Pricing Built for FFLs

EPIC ZERO uses a dual pricing framework where:

- Customers see a cash price and a credit card price at checkout

- Customers choose how they want to pay

- Card paying customers cover the cost of card acceptance

- Cash customers pay less

- The business owner does not pay per transaction card acceptance costs

- The merchant only pays any applicable monthly fees if they exist

This model allows dealers to protect margins without increasing base prices.

EPIC PLUS: Interchange Plus for Simplicity

EPIC PLUS is an interchange plus pricing model designed for dealers who want one consistent price for all customers.

With EPIC PLUS:

- Cash and card pricing remain the same

- Wholesale interchange costs pass through transparently

- EPIC’s markup is clearly disclosed

- The merchant pays per transaction processing costs

- Monthly fees are treated as standard operating expenses

Other Pricing Options

While EPIC ZERO and EPIC PLUS cover the needs of most FFLs, EPIC Merchant Systems can also support other pricing models when requested.

These may include:

• Cash discount programs

• Tiered pricing

• Flat rate pricing

• Card present versus card not present pricing

These options are typically used in specific situations and are not commonly selected by most dealers.

A knowledgeable payment partner should help you choose the right pricing structure based on how you sell and how you want to run your business, not push a one size fits all solution.

Choosing the Right Payment Setup From the Start

Payment acceptance for FFLs is not just about convenience. It is about risk management and long term viability.

Consumer payment apps may appear simple, but they introduce unnecessary exposure that can result in frozen funds, lost sales, and account termination.

A properly underwritten FFL merchant account provides:

- Predictable processing

- Compliance alignment

- Protection from sudden shutdowns

- Confidence to sell across all channels

Frequently Asked Questions

Can an FFL legally use Square or PayPal?

Some accounts may initially work, but most consumer payment platforms prohibit or restrict FFL related transactions in their policies. Shutdowns often occur after activity is reviewed.

Why do payment apps freeze funds without warning?

Payment facilitators monitor transactions after they occur and freeze funds automatically during investigations.

Is a dedicated FFL merchant account more expensive?

In many cases, no. Avoiding shutdowns, frozen funds, and lost sales often saves money long term.

Call to Action

If you are an FFL and want to accept payments without risking frozen funds or sudden account shutdowns, work with a processor that understands your industry.

Learn how EPIC ZERO and EPIC PLUS are designed to support federally licensed dealers from day one.

Talk to EPIC Merchant Systems today.