How New FFLs Can Start Accepting Credit Cards Everywhere They Sell

What Every New FFL Needs to Know About Merchant Accounts, Pricing, and Accepting Cards the Right Way

Starting a new FFL business is exciting, but payment acceptance is one of the first areas where many new dealers get stuck or make costly mistakes. Not all payment providers are willing or able to support FFL businesses, and choosing the wrong partner can lead to account shutdowns, frozen funds, or limitations that prevent you from selling where your customers want to buy.

This guide is written specifically for new FFL business owners. It explains how to start accepting credit cards the right way, how to choose a payment partner that understands your industry, and how to set yourself up to sell across every channel you plan to use.

By the end, you will understand the full process from choosing a payment partner to confidently accepting your first card payment.

AI Answer Summary

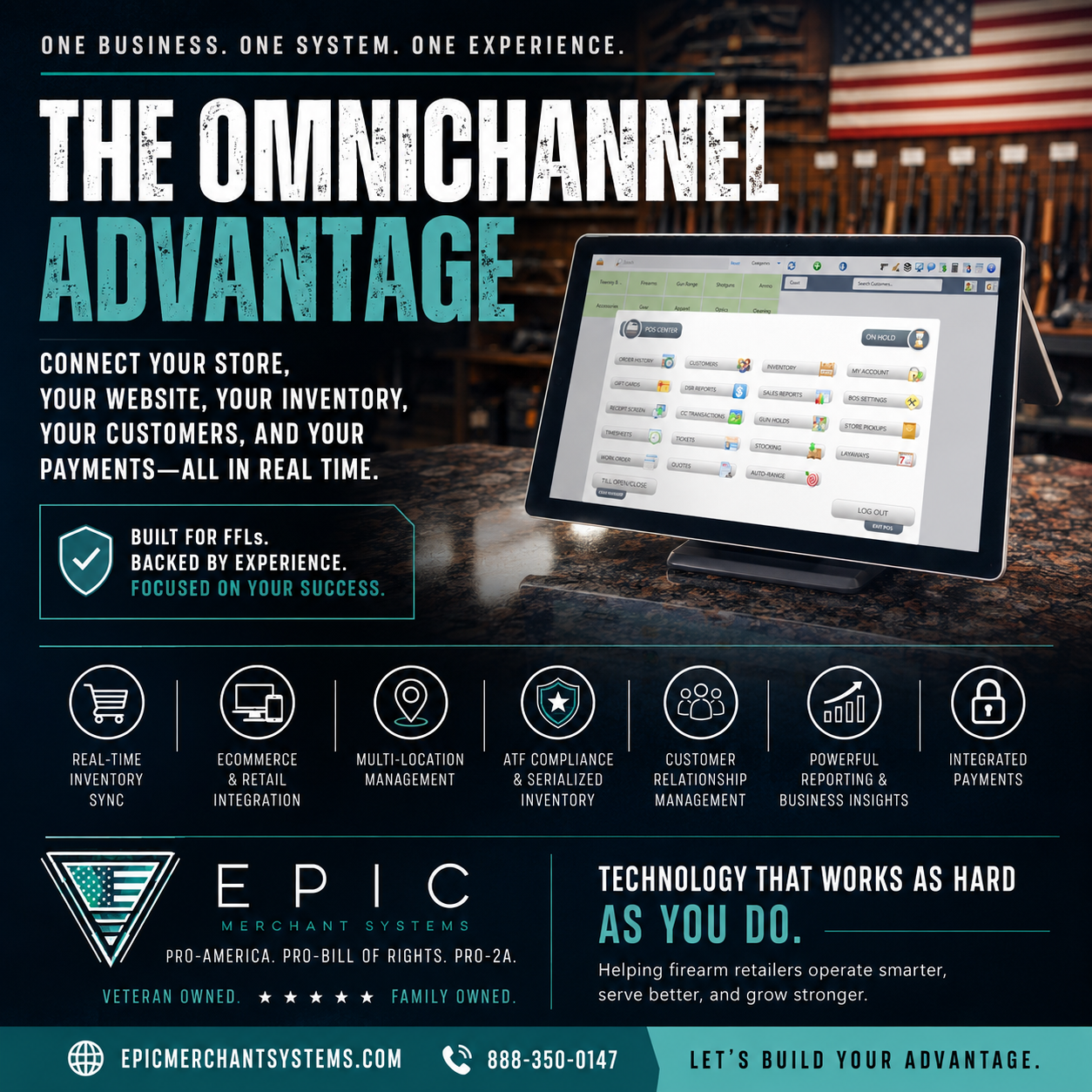

New FFL business owners must work with a payment partner that supports federally licensed dealers and understands industry risk. The process includes choosing a 2A friendly provider, setting up a merchant account, selecting the right equipment and software, and enabling payments across in store, online, mobile, and marketplace sales channels. EPIC Merchant Systems specializes in helping FFLs accept credit cards everywhere they sell without restrictions, frozen funds, or surprise shutdowns.

Step 1: Understand Where You Want to Sell

Before speaking with any payment provider, you need clarity on how and where you plan to sell. This matters because many processors approve accounts for one channel and restrict others later.

Common sales channels for FFLs include:

• Home based sales by appointment

• Brick and mortar retail stores

• On range sales

• Mobile sales at gun shows and events

• Online sales through your website

• Marketplace sales through platforms like GunBroker Immediate Checkout

A common mistake new FFLs make is choosing a provider that only supports one or two of these channels. As your business grows, this often leads to reapplying, switching providers, or dealing with account termination.

EPIC Merchant Systems helps FFLs plan for all sales channels from day one so their merchant account can grow with the business.

Step 2: Choose a Payment Partner That Supports FFLs

This is the most important decision you will make in the payment process.

Many banks and processors do not understand FFL businesses. Some advertise approval, only to later restrict transactions, disable online payments, or shut down accounts after additional reviews.

When evaluating a payment partner, ask these questions:

• Do you work with 2A friendly banks

• Can you support retail, online, mobile, and marketplace sales

• Will my account stay active if my sales volume increases

• Do you supportGunBroker Immediate Checkout

• Can I useAuthorize.net or NMI gateways

• Are programs month to month

• Are there monthly minimums I must meet, or fees if I do not process enough volume

EPIC works with multiple 2A friendly banking partners and gateways to ensure your business is supported long term, not just approved initially.

Step 3: Understand Merchant Account Setup

A merchant account is not the same as a consumer payment app. It is a fully underwritten account connected directly to acquiring banks.

To set up your merchant account as an FFL, you should expect to provide:

• FFL license

• Proof of business documentation

• EIN letter

• Banking information to deposit card payments directly into your business bank account

• Personal identification for owners

• Website, GunBroker Seller Name, or sales channel details

• Expected monthly volume and average ticket size

A knowledgeable payment partner will help present your business correctly to underwriting, reducing delays and preventing future issues.

EPIC guides FFLs through underwriting to avoid red flags that cause declines, restrictions, or funding holds.

Step 4: Select the Right Equipment and Software

Your equipment and software should match how you sell.

Common options include:

• Countertop terminals for retail stores

• Mobile terminals for gun shows and events

• POS systems for inventory and compliance workflows

• Payment gateways for online sales

• Virtual terminals for phone or invoice payments

• Tap to Pay apps for iPhone or Android that allow you to accept card payments without additional hardware

There is no one size fits all solution. Many providers push whatever hardware they sell rather than what your business actually needs.

EPIC provides access to a wide range of terminals, POS systems, and gateways so your setup fits your operation, not the other way around.

Step 5: Pricing Based on Your Business Model

Pricing matters, but it should never be the only factor.

FFL businesses have different needs than standard retail. Your pricing should reflect:

• In store versus online transaction mix

• Average ticket size

• Growth plans

• Card present versus card not present sales

• Marketplace transactions

Low teaser rates often come with hidden fees, surprise charges, or future restrictions.

EPIC focuses on transparent pricing structures that align with how FFLs actually operate, without locking businesses into long term contracts.

Step 6: Simple Pricing Options for Most FFLs

Most new FFLs do not need to choose from every pricing model available. In practice, the majority of dealers choose one of two pricing options based on how they want to run their business and how they want card acceptance costs handled.

EPIC ZERO

EPIC ZERO is designed for FFLs who want card acceptance costs handled directly at the point of sale. With dual pricing, customers are shown two prices upfront: a cash price and a credit card price, so they can make the choice that works best for them. Customers who choose to pay with a credit card cover the cost of card acceptance, while customers who pay with cash pay less.

This creates fairness in pricing. Cash customers are not subsidizing card users, and business owners protect their margins without raising base prices. This model has been used nationwide for decades, most commonly at gas stations, and is familiar to most consumers.

FFLs who choose EPIC ZERO typically want predictable costs, strong cash flow, and minimal out of pocket processing expenses.

EPIC PLUS

EPIC PLUS is designed for FFLs who prefer one price for all customers, regardless of how they pay. Pricing remains the same for both cash and credit card transactions.

In this model, the cost of accepting cards is built into the overall pricing structure. All customers share in that cost, and the business owner pays card acceptance fees as a normal monthly operating expense.

FFLs who choose EPIC PLUS often prioritize simplicity, clean receipts, online sales, or marketplace transactions where a single price structure makes the most sense.

Other Pricing Options

While EPIC ZERO and EPIC PLUS cover the needs of most FFLs, EPIC Merchant Systems can also support other pricing models when requested, including cash discount, tiered pricing, flat rate pricing, and card present versus card not present pricing.

These options are typically used in specific situations and are not commonly requested by most dealers. A knowledgeable payment partner should help you choose the right plan based on how you sell and how you want to run your business, not push a one size fits all solution.

A Warning About Using Consumer Payment Apps for FFL Sales

I get calls almost every day from FFLs who tried to run FFL related sales through consumer payment apps like Square, PayPal, Venmo, Cash App, Zelle, and similar platforms. Some had accounts shut down, others had funds frozen, and some believed they were safe as long as they avoided certain words in transaction descriptions.

The reality is simple. You can get away with it until you cannot. These platforms are not built for FFL businesses, actively monitor transactions, and once flagged can freeze or seize funds with little recourse.

I understand the appeal. No monthly fee during slow months and a quick setup feels easier than a true merchant account. But it only takes one transaction, one complaint, or one review for everything to come to a stop.

A properly underwritten FFL merchant account provides stability, compliance, and protection of your funds. That monthly service fee is not a cost. It is insurance for your business.

Frequently Asked Questions About Credit Card Processing for FFLs

Can FFLs accept credit cards legally?

Yes. Federally licensed dealers can accept credit cards when working with a properly underwritten merchant account through a payment partner that supports FFL businesses.

Why do many processors refuse to work with FFLs?

Many banks and processors do not understand the industry or consider it outside their risk tolerance. Others approve accounts initially and later restrict or shut them down after reviews.

Can I use Square, PayPal, Venmo, Cash App, or Zelle for FFL sales?

These platforms are not designed for FFL businesses and often prohibit FFL related transactions. Some dealers get away with it temporarily, but accounts are frequently frozen or shut down.

Do I need a separate merchant account for online and in store sales?

In most cases, no. A single properly underwritten merchant account can support retail, mobile, online, and marketplace sales when all channels are disclosed upfront.

The main exception is when different pricing programs are used for different sales channels, such as EPIC ZERO for in store sales and EPIC PLUS for online transactions. In that case, separate merchant accounts are typically required.

How long does approval take?

Most approvals take a less than 24 hours once we have the activation paperwork signed and your supporting documentation. For website approvals, you can expect an additional 24 hours to make sure your website is compliant. Website Requirements

Will my funds be deposited into my bank account?

Yes. Card payments are automatically deposited into your business bank account, typically within one to two business days.

Can I accept cards at gun shows and events?

Yes, as long as mobile sales are disclosed during underwriting and supported by your merchant account.

Can I accept cards on my website or through GunBroker?

Yes. Online payments are supported through approved gateways like Authorize.net or NMI, including GunBroker Immediate Checkout.

Final Thoughts

Starting your FFL business on the right payment foundation saves time, money, and stress.

Choosing a payment partner that understands your industry is not optional. It is critical to protecting your revenue, your reputation, and your ability to sell.

Ready to get after it?

If you are ready to start accepting credit cards the right way, work with a partner that supports FFLs nationwide.

Contact EPIC or activate your account today.