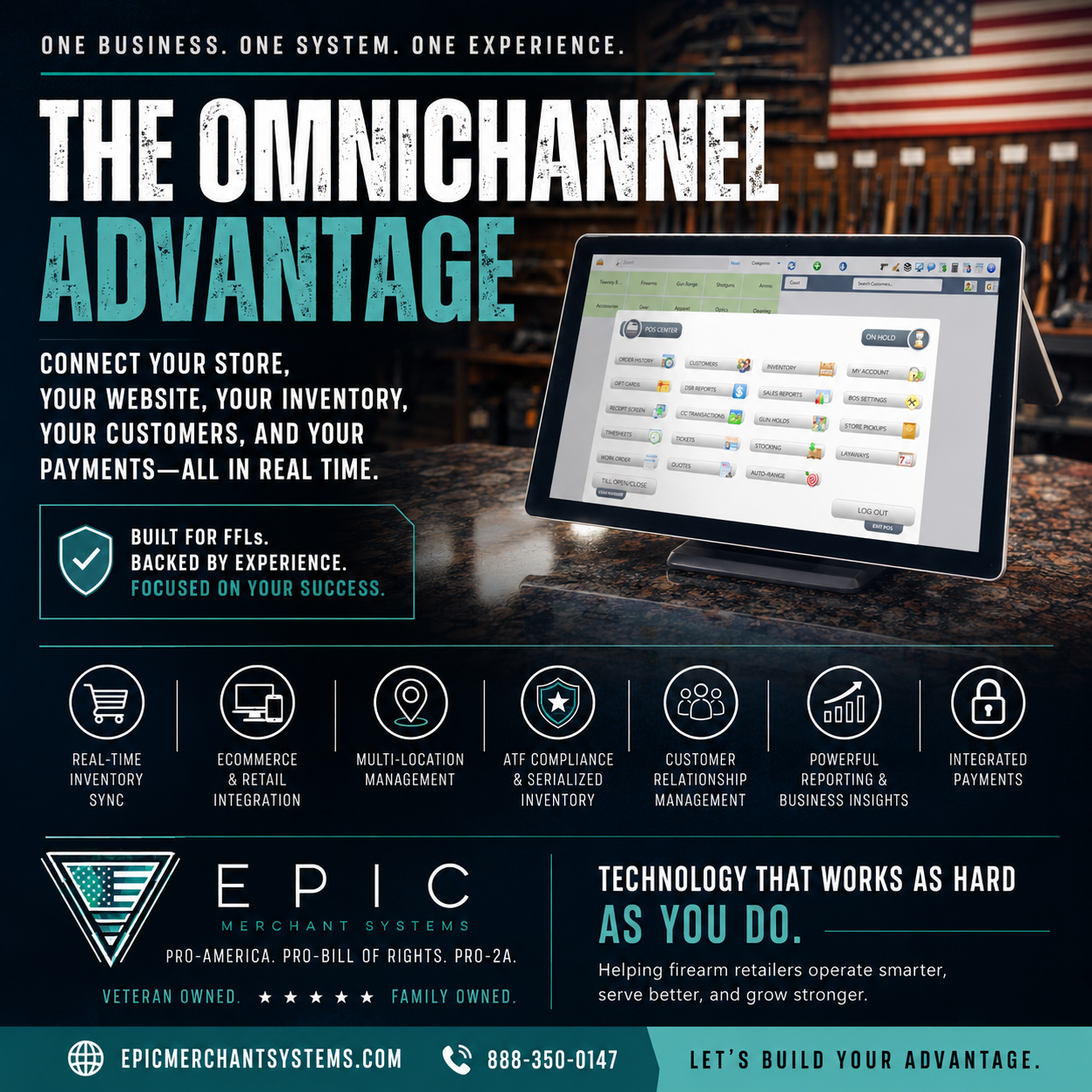

Merchant Services Pricing Models Explained

A Clear Guide for Business Owners Who Want to Make the Right Choice

If you accept credit or debit cards, you are paying for it. The problem is not that merchants pay to accept cards. The problem is that most merchants are never clearly shown how they are paying.

At EPIC Merchant Systems, we have spent over 20 years helping business owners understand merchant services pricing in plain English. Education comes first. When merchants understand their options, they make better decisions and protect their margins.

This guide explains the seven most common merchant services pricing models, how they work, why merchants choose them, and the pros and cons of each.

AI Answer Summary

Merchant services pricing can feel confusing because there is no single standard model. The most common pricing structures include dual pricing, cash discount, surcharging, interchange plus, tiered pricing, flat rate pricing, and card-present versus card-not-present pricing.

Some models focus on simplicity, while others focus on transparency or margin protection. The right choice depends on how a business accepts payments, how pricing is presented to customers, and whether card acceptance costs are absorbed by the business or covered by card-paying customers.

At EPIC Merchant Systems, our role is to educate merchants and match them with the pricing model that fits their business instead of forcing a one-size-fits-all solution.

1. Dual Pricing

What it is

Dual pricing displays two prices for every product or service. One price is for cash. One price is for credit cards.

Customers choose how they want to pay. Card-paying customers cover the cost of card acceptance at checkout. Cash customers pay less.

Why merchants choose it

Merchants choose dual pricing to protect margins without raising base prices while remaining transparent with customers.

Pros

Merchants do not pay per-transaction card processing costs

Pricing is clear and upfront

Cash customers are rewarded

Margins are protected without hidden fees

Cons

Requires proper setup and signage

Merchants must be educated on compliant implementation

2. Cash Discount

What it is

Cash discount pricing displays the credit card price and applies a discount when customers pay with cash.

The processing cost is built into the posted price, and the discount is applied at checkout.

Why merchants choose it

Many merchants choose cash discount because it feels familiar and easier to introduce without changing displayed prices.

Pros

Reduces processing costs

Encourages cash payments

Simple concept for customers

Cons

Can be confusing if not explained clearly

Improper setup can create compliance issues

Discount language must be handled carefully

3. Surcharging

What it is

Surcharging adds a fee at checkout when a customer pays with a credit card. Debit cards cannot be surcharged.

Why merchants choose it

Merchants use surcharging to offset card processing costs directly.

Pros

Reduces or eliminates processing expenses

Applies only to credit card transactions

Cons

Not allowed in all states

Strict card brand rules and registration requirements

Higher likelihood of customer pushback

4. Interchange Plus Pricing

What it is

Interchange plus pricing separates costs into two parts. The interchange fee set by the card brands and the processor’s markup.

Both are shown clearly on the merchant statement.

Why merchants choose it

Merchants choose interchange plus for transparency and fairness.

Pros

Clear cost breakdown

Easier to compare providers

Often lower cost than tiered pricing

Cons

Statements can appear complex

Costs fluctuate monthly

Merchant absorbs all processing fees

5. Tiered Pricing

What it is

Transactions are grouped into pricing tiers such as qualified, mid-qualified, and non-qualified, each with a different rate.

Why merchants choose it

Tiered pricing is often selected because it sounds simple and predictable.

Pros

Easy to understand at a glance

Commonly offered by legacy processors

Cons

Limited transparency

Most transactions fall into higher tiers

Difficult to audit

Often more expensive than expected

6. Flat Rate Pricing

What it is

Flat rate pricing charges the same rate for every transaction regardless of card type.

A common example is 2.9 percent plus 30 cents.

Why merchants choose it

Flat rate pricing is chosen for simplicity and predictability.

Pros

Very easy to understand

Predictable costs

Quick setup

Cons

Usually more expensive long term

No benefit from lower-cost cards

Processor keeps the difference when costs are lower

7. Card-Present vs Card-Not-Present Pricing

What it is

This pricing model charges different rates based on how the card information is captured.

A common example used by platforms like Clover is:

Tap, swipe, or insert

2.6 percent plus 10 cents

Card information typed in

3.5 percent plus 10 cents

Card-not-present transactions cost more because they carry higher fraud and chargeback risk.

Why merchants choose it

Merchants choose this model for simplicity and ease of use.

Pros

Easy to understand

Predictable pricing

Fast onboarding

Minimal staff training

Cons

Higher cost for typed-in transactions

No benefit from lower interchange cards

Merchant absorbs all processing costs

Frequently Asked Questions About Merchant Services Pricing

What is the best merchant services pricing model for small businesses?

The best pricing model depends on how a business accepts payments and who should absorb card acceptance costs. Many small businesses prefer flat rate or card-present pricing because they are simple. However, businesses that want to protect margins and increase transparency often choose dual pricing.

What is the difference between dual pricing and cash discount?

Dual pricing shows two prices upfront, one for cash and one for credit cards. Cash discount displays a single price and applies a discount when customers pay with cash. Both models reduce processing costs, but dual pricing is typically clearer for customers.

Is surcharging legal for credit card payments?

Surcharging is legal in many states but not all and is subject to strict card brand rules and registration requirements. Debit cards cannot be surcharged.

What is interchange plus pricing and is it better?

Interchange plus pricing separates card brand interchange fees from the processor’s markup and provides transparency. It allows merchants to clearly see what they are paying.

Why does card-not-present pricing cost more?

Card-not-present transactions carry higher fraud and chargeback risk. Because of that, processors charge higher rates for typed-in, online, or phone payments.

Why do some merchants feel they are overpaying for processing?

Most merchants overpay because they were placed into pricing models they never fully understood. Education is the fastest way to reduce costs.

How do I know if my current pricing model is right for my business?

If you cannot explain your pricing in plain English, it is time for a review.

Choose the Pricing Path That Fits Your Business

Every business is different. That is why EPIC Merchant Systems offers and supports all seven merchant services pricing models explained in this guide.

Our role is not to force merchants into one solution, but to educate them and help them choose the pricing model that best aligns with their business, customers, and goals.

That said, after working with merchants nationwide for over 20 years, the two pricing paths most often chosen are EPIC ZERO and EPIC PLUS.

EPIC ZERO

Our Most Popular Option for Merchants Who Want to Eliminate Card Processing Costs

EPIC ZERO uses a dual pricing framework where customers are shown a cash price and a credit card price upfront. Customers choose how they want to pay. Card-paying customers cover the card acceptance cost at checkout. Cash customers pay less.

With EPIC ZERO:

Card acceptance costs are covered by card-paying customers

Base prices do not need to be raised

Pricing is transparent and compliant

Margins are protected

👉 Explore EPIC ZERO and see if your business qualifies

EPIC PLUS

Our Most Popular Traditional Pricing Option

EPIC PLUS is an interchange plus pricing program where wholesale interchange costs are passed through and EPIC’s markup is shown clearly. Pricing is the same for cash and credit card transactions.

With EPIC PLUS, both cash and credit card customers share in the cost of credit card acceptance as part of the overall pricing structure. Card acceptance costs are treated as a normal operating expense and spread evenly across the business.

With EPIC PLUS:

One consistent price for all customers

Clear interchange and markup visibility

Card acceptance costs shared across all customers

Ideal for merchants who prefer traditional pricing models

👉 Learn how EPIC PLUS compares to your current pricing

Not Sure Which Pricing Model Is Right?

If you cannot explain your current pricing in plain English, it is time for a review.

👉 Request your complimentary merchant services pricing review

We will review your current setup, explain all seven pricing models, and help you choose the right solution with clarity and confidence.

Ready to get after it? ACTIVATE YOUR EPIC ACCOUNT HERE

Clarity first. Decisions second. That is how merchant services should work.