New FFL Payment Processing Explained: How to Accept Credit Cards Without the Confusion

Starting a new FFL business is exciting. But when it comes time to accept credit cards, many new license holders feel completely lost.

You hear different answers from different providers.

Some say it is easy.

Others warn you it is “high risk.”

Fees, contracts, gateways, terminals, and compliance rules are thrown at you, often without clear explanations.

The truth is this:

Most FFLs do not struggle with payment processing because they are doing something wrong. They struggle because no one explains how payment processing actually works for their type of business.

This guide breaks down FFL payment processing in plain language so you can accept credit cards confidently whether you operate from home, a storefront, events, online, or marketplaces like GunBroker.

Why Payment Processing Is Different for FFLs

Accepting credit cards as an FFL is not the same as running a coffee shop or a retail boutique.

Even though your business is legal, banks and card networks apply additional risk rules to FFLs. These rules affect:

- Approval requirements

- How transactions are monitored

- Which sales channels are allowed

- Which gateways and hardware can be used

Many new FFLs run into trouble because they sign up with a processor that does not fully understand these rules. The result is often frozen funds, surprise account reviews, or full account shutdowns.

The key is not avoiding credit cards.

The key is setting things up correctly from the start.

The Different Ways FFLs Accept Payments

One of the biggest mistakes new FFLs make is assuming all sales channels are treated the same.

They are not.

Each sales channel carries different risk and technical requirements.

Home-Based FFL Payment Processing

Yes, home-based FFLs can accept credit cards.

Approval typically depends on:

- Proper business documentation

- An accurate description of how sales occur

- Clear disclosure of products and sales channels

Problems arise when home-based FFLs try to look like retail storefronts or use generic processors that are not FFL-friendly.

Retail Storefront Payment Processing

Retail FFLs usually have the lowest risk profile, but they still require:

- FFL-approved merchant accounts

- Proper terminal configuration

- Correct product and transaction coding

Retail setups done incorrectly often trigger increased monitoring or future restrictions.

Mobile and Event Payment Processing

FFLs selling at:

- Gun shows

- Events

- Temporary locations

Need mobile payment solutions that are approved for FFL use.

Using consumer apps or unapproved mobile readers is one of the fastest ways to get a merchant account shut down.

Ecommerce Payment Processing for FFLs

Online sales introduce higher scrutiny due to:

- Card-not-present transactions

- Increased fraud exposure

- Higher chargeback risk

Ecommerce FFLs must use the correct payment gateway and ensure their website aligns with underwriting expectations.

Marketplace Sales Including GunBroker

Marketplaces like GunBroker add another layer of complexity, including:

- Marketplace-specific payment requirements

- Approved gateways for Immediate Checkout

- Proper transaction flow between buyer, seller, and processor

Many FFLs get stuck here because their processor says “yes” without actually supporting marketplace requirements.

Common Mistakes New FFLs Make

After working with FFLs nationwide, these mistakes come up again and again:

- Signing up with processors that claim they support FFLs but do not

- Failing to disclose all sales channels upfront

- Mixing retail, mobile, and online sales incorrectly

- Using the wrong gateway or terminal

- Choosing the lowest advertised rate instead of the safest setup

These mistakes are rarely intentional. They are caused by confusion and lack of guidance.

Before you sign Anything

Before choosing a processor, it is worth talking to someone who understands how FFL payment processing actually works. One short conversation can prevent months of frustration.

[Talk to an FFL Payment Specialist]

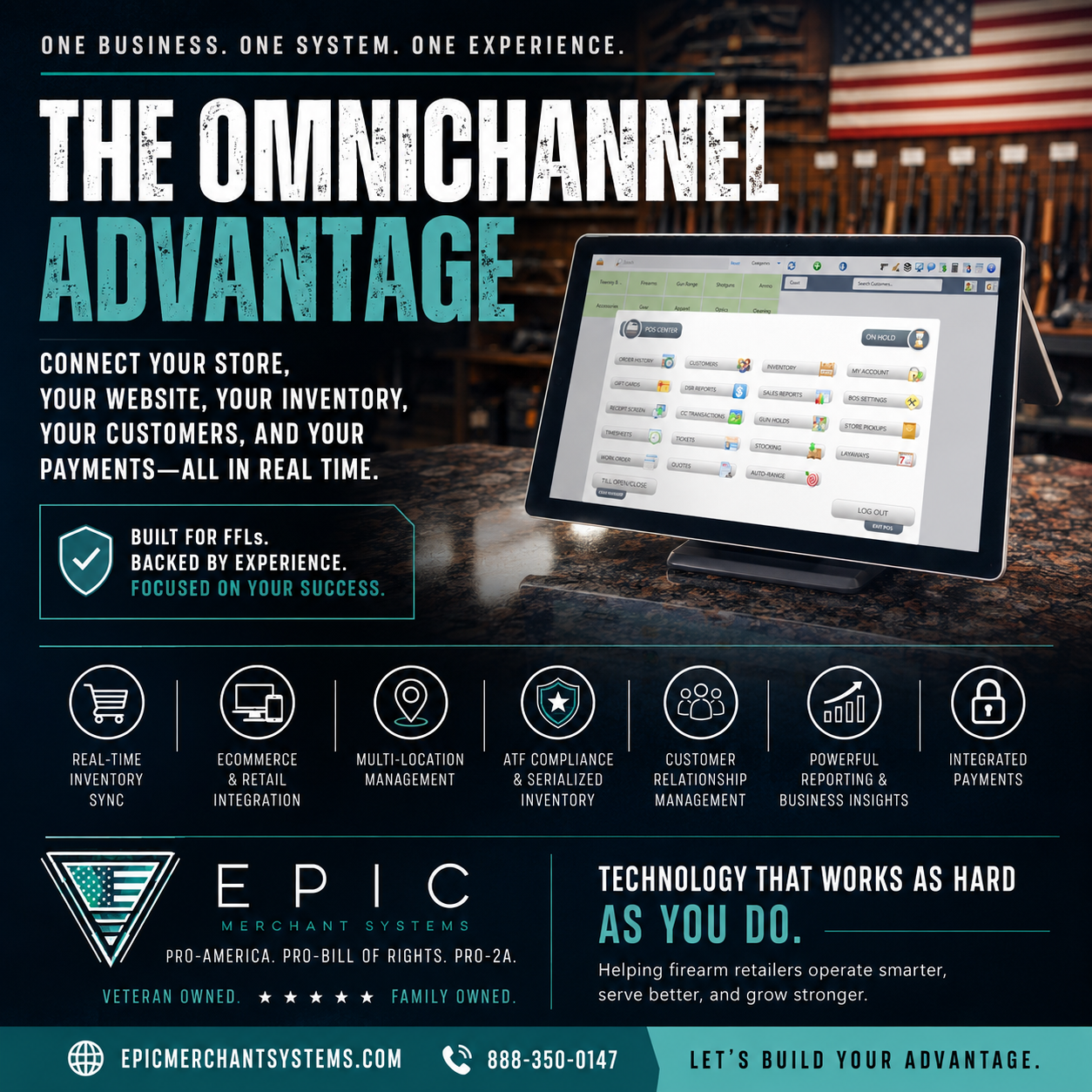

How EPIC Merchant Systems Keeps It Simple

At EPIC Merchant Systems, our approach is straightforward.

We do not force FFLs into one-size-fits-all solutions. We design payment setups based on how you actually do business.

We help FFLs with:

- Home-based, retail, mobile, ecommerce, and marketplace setups

- FFL-approved merchant accounts

- Proper underwriting from day one

- Approved gateways, including GunBroker-compatible options

- Clear explanations with no jargon

Most importantly, you work with real people who understand FFL businesses, not a call center reading from a script.

What to Look for in an FFL Payment Processing Partner

Before choosing a provider, make sure they can answer these questions clearly:

- Do you support home-based, retail, mobile, and online FFLs?

- Are your merchant accounts truly FFL-approved?

- Can you support marketplaces like GunBroker properly?

- Will my sales channels be disclosed and approved upfront?

- Do I have a real point of contact if something goes wrong?

If a provider cannot answer these confidently, that is a red flag.

Frequently Asked Questions About New FFL Payment Processing

Can a new FFL accept credit cards right away?

Yes. New FFLs can accept credit cards as soon as their business is properly set up and approved by an FFL-friendly processor.

Can a home-based FFL accept credit cards?

Yes. Home-based FFLs are eligible, but the setup must accurately reflect how and where sales occur.

Do I need separate merchant accounts for retail and online sales?

In many cases, yes. Retail and ecommerce transactions are evaluated differently, and separating them often reduces risk.

Why do FFL merchant accounts get shut down?

Most shutdowns occur due to undisclosed sales channels, incorrect gateways, or processors that are not truly FFL-friendly.

Can I accept payments on GunBroker?

Yes, but you must use an approved gateway and a processor that supports GunBroker transaction flows.

How long does FFL payment processing setup take?

When done correctly, approval typically takes a few business days once all documentation is submitted.

Get Guidance Before You Sign Anything

If you are a new FFL or an existing one that feels overwhelmed, you do not need to figure this out alone.

At EPIC Merchant Systems, we specialize in helping FFLs accept credit cards the right way, without confusion, hidden surprises, or unnecessary risk.

Before you sign a contract or choose a processor, talk to someone who understands your business.